When it comes to stock market investment strategies for 2025, striking the right balance between growth and stability is key. Recently, a client shared a Vanguard article suggesting that high stock market valuations, based on PE ratios, signal it’s time to shift from a 60/40 portfolio (60% stocks, 40% bonds) to a 70% bond, 30% stock allocation. Their reasoning? They expect stocks to return just 3.3% to 5.3% over the next decade, while bonds could yield 4% to 5% risk-free. But is this the best approach? In our latest discussion, Grayson Shaw and Stephen Hammond analyze historical data, market trends, and why betting against the S&P 500 could be risky. Whether you’re a retiree, a young investor or somewhere in between, this post offers insights into optimizing your stock market investment strategies.

Vanguard’s Outlook: High Valuations and a Call for Caution

Grayson: A client sent us an article from Vanguard. They argued that based on PE valuations, the stock market is too high. For investors with a 10-year time horizon, they recommend switching from a 60/40 split (60% stocks, 40% bonds) to 70% bonds and 30% stocks. They expect stocks to increase only about 3.3% to 5.3% over the next 10 years, with bonds delivering 4% to 5% risk-free.

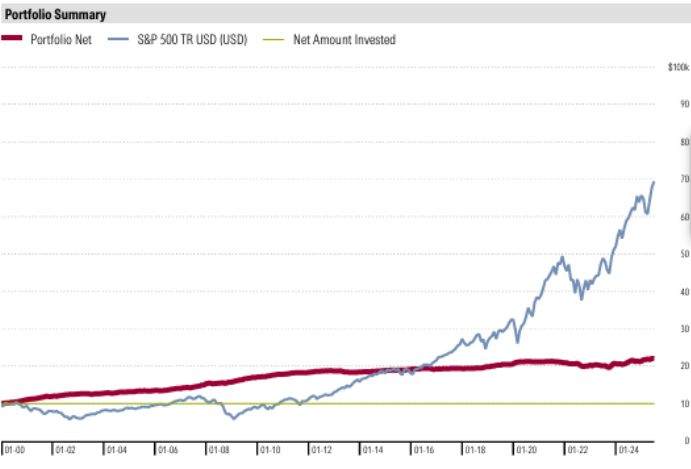

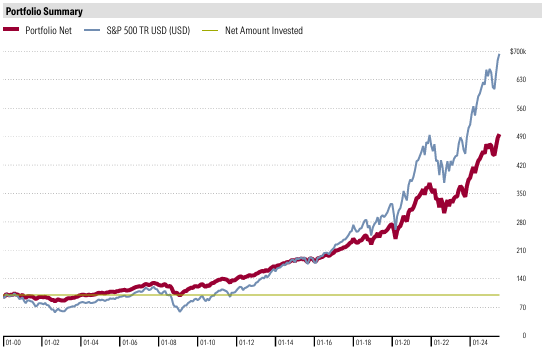

Stephen: I think most of the time, this strategy won’t work. We analyzed data since 1929, covering 86 rolling 10-year periods through 2023. Only five times did a 70% bond, 30% stock mix outperform the S&P 500. That means 94% of the time, you’re better off with the S&P 500 than being heavily weighted in bonds for your stock market investment strategies.

The Pitfalls of Relying on Metrics Like the Schiller PE Ratio

Grayson: They mentioned the Schiller PE ratio in the article, haven’t you taken that into consideration in the past?

Stephen: I used to rely on that until about 2012-2013. It doesn’t work anymore. Vanguard might think the S&P is lofty and could retreat due to debt or other factors. But betting against the S&P over a 10-year rolling period is not a smart move for most investors’ stock market investment strategies.

Grayson: You said 94% of the time you’d lose on this bet. Maybe if you’ve done your homework—like timing the market with valuations—it could work if it’s proven. But things have changed over the last 15 years, with money from other countries flowing into US equities.

Stephen: Yes, I like to joke with people and tell them that my crystal ball broke around 2012, and I haven’t fixed it. Tools from 1987 to 2013 don’t work anymore — international investors are pouring into the US market since it’s the best place to invest. Old strategies don’t apply as much as they used to, so relying on valuations for when to get in and out of the market isn’t a good strategy any longer.

Bonds in Your Portfolio: Safe Haven or Growth Killer?

Grayson: Bonds have traditionally been a safe haven when the market underperforms. Is there still a place for them? Some say there’s no alternative to stocks. What should investors do based on risk tolerance— whether retirees or young people aiming for yields over the course of 30 years?

Stephen: Asset allocation is critical. A 70% bond portfolio is simply too much. A 40% bond allocation post-retirement—a 60/40 split—is solid. We hedge portfolio risk with short-term bonds, and in a decreasing interest rate environment, we’ll lengthen maturities. Bonds generate income and stabilize your portfolio, but too many bonds can choke growth. Learn more about bond hedging strategies.

Current Market Headwinds: Interest Rates, Valuations, and Growth Potential

Grayson: Interest rates are likely to be cut within six months, which is good for equities, there don’t seem to be many headwinds for the economy or stock market — can you see any reason to flee stocks now?

Stephen: Valuations are high, but there’s room for growth. It’s possible we could see a 5-10% market dip which could be healthy for the stock market. The market anticipates things like a Federal Reserve rate cut in September, and a post-cut selloff could occur, and that’s fine. Regular market fluctuations are typical, but being out of the stock market can end up costing you.

Grayson: So, in short, avoid the 30/70 split with 70% bonds. It’s not ideal for keeping up with inflation, growing your portfolio, or leaving a legacy.

Stephen: Absolutely.

Final Thoughts: Stick with Balanced Asset Allocation for Long-Term Success

Vanguard’s caution on valuations is worth noting, but historical data strongly favors the stock market for long-term returns. A heavy bond tilt might feel safe but could limit growth, especially with rate cuts boosting stocks. Tailor your stock market investment strategies to your risk tolerance—consider a 60/40 mix for balance—and avoid extreme shifts. For personalized advice, contact our team or explore our retirement planning guide.